Cryptocurrencies have been around for over a decade, and interest in them has been growing year by year. In fact, new digital currencies are hitting the market nearly every day. Following the paths of innovation, many are starting to take an interest in the field of blockchain and cryptocurrencies. This guide is for all of you looking to build your crypto-related projects.

In this article, you will learn how cryptocurrencies work and how to create a cryptocurrency of your own. We will go through the best solutions, differences between tokens and coins, nodes, token economics and everything else you might need along the way. The goal here is to give you a clearer image of modern digital currencies, explain their pros and cons, and finally, to enable you to create your own digital coin and maybe dive into the adventure in our industry.

What Is a Cryptocurrency?

Many people aren’t even sure what cryptocurrencies are. So, for those that don’t know what digital currencies are yet, we will give a quick explanation. For those that are past this level, don’t worry, by the end of the article, practical things are coming a bit down the road.

In short, cryptocurrencies are digital assets meant to function as a medium of exchange and store of value. Each cryptocurrency uses strong cryptography as a way of ensuring security during transactions. The same decentralized cryptographic systems are also in charge of creating new units and verifying transfers. The main idea behind digital money is decentralization, transparency, and immutability.

Decentralization means that there is no organization or individual in charge of everything, as is the case with regular banks and fiat currencies. Instead of using central authority, digital currencies use consensus where users have the right to vote and decide on the matters relevant to the network. The underlying technology of cryptocurrencies is blockchain.

According to Wikipedia, blockchain is a growing list of records, called blocks, that are linked using cryptography. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. By design, a blockchain is resistant to modification of the data.

Every transaction is recorded on computers in the network (also called “Nodes”, remember that word). All transactions that happen in the network are stored in the blocks, and those blocks make a blockchain. The control of the network is decentralized, blockchains are immutable and (typically) transparent (meaning that anyone can see the transactions, but not any personal information about the participants). So, while transparency is an integral part of digital money, you should not confuse it with a lack of privacy.

Similarly to other forms of currencies, users pay fees for each transaction. However, with crypto, the fees are lower, regardless of whether you are transferring small or large sums of money.

While this might seem less secure since there is no one to observe the whole process, the reality is quite different. It’s not that nobody is in charge, it’s that we all are. That’s the beauty of the blockchain, cryptocurrencies have democratized governance and actually put the power in the hands of users.

How Does Cryptocurrency Work?

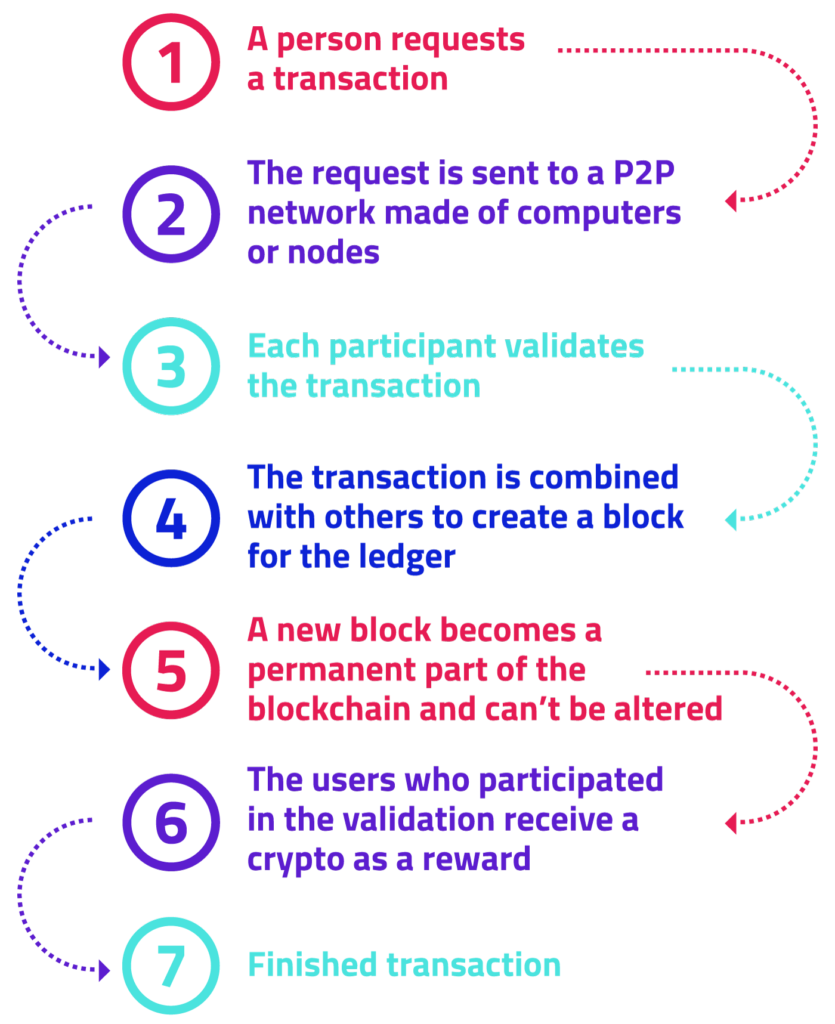

Most digital currencies are based on blockchain technology. Of course, there are also those that don’t rely on blockchain, but either on centralized or other types of decentralized solutions. What’s important to note is that Blockchain stores every information and transaction since the origin of the digital coin. And the reason why it is considered immutable is that these blocks of information cannot be altered in any way without changing all subsequent blocks. This mechanism doesn’t make hacking impossible per se, but it does make it really costly, as it requires immense amounts of computing power and time without guarantees it would work.

A consensus mechanism is in charge of validating and regulating the creation of new blocks. Whenever a new one originates, all participants of the P2P network will have to accept it before it becomes part of the blockchain. The consensus algorithm basically works by making sure that the distributed nodes in the network have to agree on the validity of any given transaction for it to be accepted. The most popular and common ways of accepting or validating a block are proof-of-work (PoW), proof-of-stake (PoS), and proof-or-authority (PoA).

Each of these consensus mechanisms works in a different way. For example, in PoW, each node that locks the block onto the blockchain gets rewarded in a form of new coins. In PoS, holding coins in the wallet will generate new coins for you. These users will spend their resources, such as their computer processing power, to support the network and will receive crypto in return. They can later either use it for shopping, exchange it for fiat money, trade it, and so on.

Pros and Cons of Building Your Own Cryptocurrency

Of course, there are pros and cons you should consider before you decide to make your own digital coins or tokens. Here, we will go through all the ups and downs of cryptocurrencies in general as well as the advantages and disadvantages of creating your own coin or token. This way, you’ll have an easier time figuring out if it is a good idea to do it yourself.

Advantages of Cryptocurrency

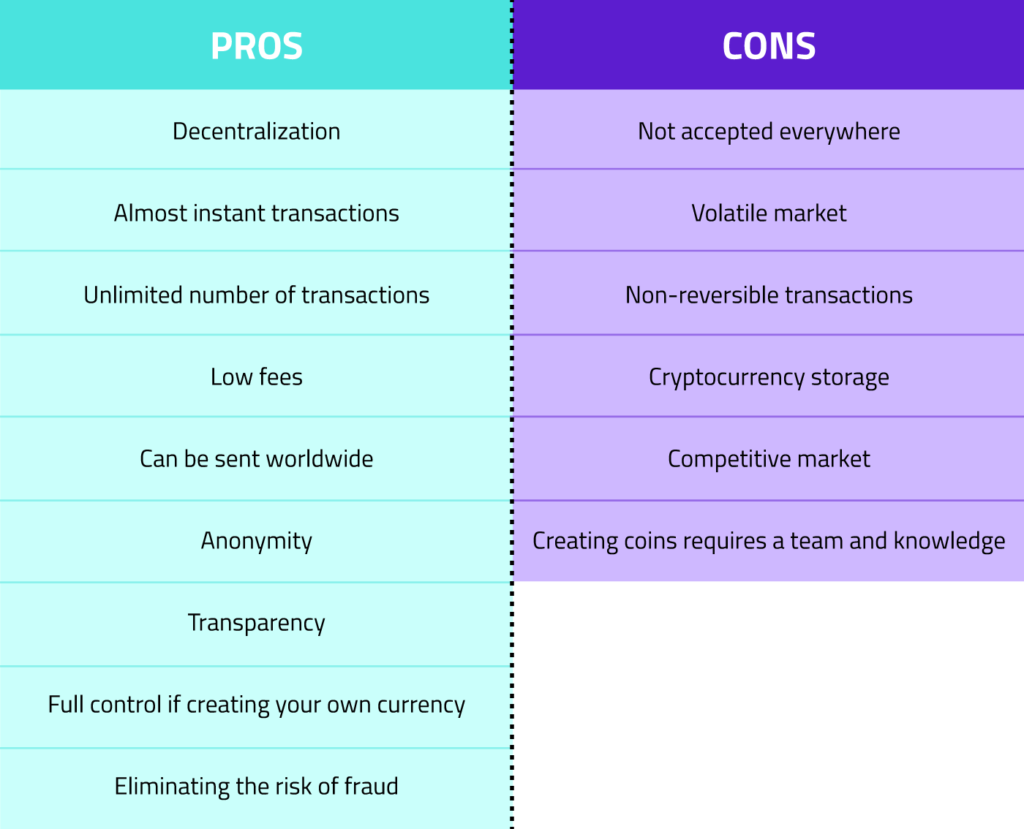

The first and most obvious advantage is decentralization. Since this type of digital asset is not dependent on any authority, it means that no one can abuse the system and dictate the rules. This means that there will never be a sudden, unexpected change of plans, and you won’t suffer for not reading the fine print.

Second, with regular fiat money, the transaction processing time is too long. You are probably aware of the fact that receiving money sometimes takes several days. However, with digital money, all transactions are nearly instant. In addition, there is no limit on how much money you can transfer, nor will you have to pay percentage fees. Banks have rather high fees, and sending large sums means they get even higher. With cryptocurrencies, transactions usually cost a lot less than one percent of the total transaction value.

Also, banks will require you to fill out forms, do the whole calculation, and figure out the complicated logistics if you are looking to send money out of the country. There are additional codes, fees, making the whole process difficult and time-consuming. Cryptocurrencies, on the other hand, are accepted internationally. Not only will you not have to worry about exchange fees for different currencies, but you can also send money to any part of the world. Aside from standard fees, international ones can get rather high if you are using banks and services like Western Union. Another benefit of digital currencies lies in anonymity and transparency as no one will know who the sender is or who received the money.

If we’re talking about your own digital cash, you’ll have full control over the direction in which it will evolve. This way, you will be able to avoid declines in the value of your money while you are potentially filling the gap in the market.

Disadvantages of Cryptocurrencies

Naturally, not everything is puppies and rainbows, and there are many disadvantages to using non-fiat money. Firstly, most governments are not fond of this type of transaction, and you will face limited acceptance using any of the cryptocurrencies available on the market (depending on your location). Also, people often don’t even realize how they could use them at all.

Also, the whole market is highly volatile. Investing in cryptocurrencies is considered a high-risk endeavor, especially if you lack experience and familiarity with the market. Keep in mind that transactions are not reversible, so if you made a mistake there are no guarantees you’ll be able to get your money back. While there is sometimes an option to ask for a refund, you can only hope that the other party will accept it.

Another disadvantage is complicated security. While all transactions are secure, it is not rare that people lose their keys, devices, or forget their login details. You won’t be able to go to the bank and show your ID to get access to your digital wallet.

Recently, there’s been so much talk about Bitcoin, Ethereum, NEO, and all other altcoins (all coins that aren’t Bitcoin), and it’s obvious that the competition is strong. If you create your own digital cash, you should know that the market is quite competitive. There are over 6,000 different coins and tokens, and sometimes, making your own might not give you the financial benefit you’d expect.

Finally, building your own blockchain will require a full-time commitment, which might be too much if you don’t have a team to back you up.

The Difference Between Tokens and Coins

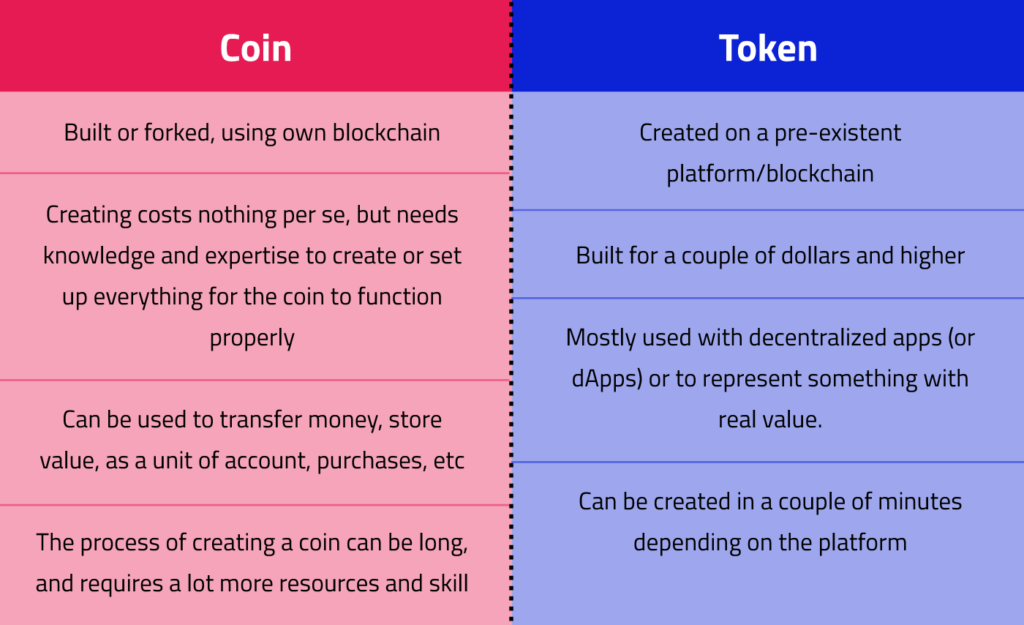

There are two main types of digital currencies — tokens and coins. The main purpose of coins is the same as that of fiat money – you can buy services or goods with them, save them, or almost anything else you can do with real money. The main thing about the coins is that they have their own blockchain.

The examples of coins are Bitcoin or Dash. Each of these has its own blockchain that contains all transactions. So if you are looking to make a new coin, you might want to think about creating your own blockchain as well.

On the other hand, tokens don’t have their own blockchain; they use existing platforms instead. An example of this is the ERC-20 token standard, which was developed by the Ethereum platform. With ERC-20 you can create your own token in a matter of minutes. Naturally, Ethereum is not the only platform offering this type of service. NEO, Waves, Stellar, and several other platforms allow easy creation of tokens as well. platforms that allow users to create their own tokens.

The Business Model Behind the Making of a Cryptocurrency

Before we dive into the technical aspect of creating digital coins, you should consider creating at least an outline of the business process first. Whether you have a business already, or you plan on creating one, you should know how your coin should fit into the whole picture. You can opt for tokens, or you can create coins. We have already mentioned that creating a coin is a bit more complex and that you may need a team to do it properly.

Define the Idea

The first step is to ask yourself how this new currency will fit into your business. What problems are you looking to solve with a decentralized currency or application? What is your target audience?

Your main goal should be to design a token economy around your business model that has clearly defined value streams to incentivize all network participants to act in good faith and ensure system stability around your product or service. When you have this core idea planned out, you can start thinking about fundraising for your project.

Initial Coin Offering

One of the most common methods many cryptocurrency projects have used to create interest and raise funds was an ICO (Initial Coin Offering). Although the Initial Coin Offerings are nowadays less popular than a couple of years ago, it’s still one of the ways to get funds for your new project. The idea behind ICOs is to find outside help or funds. The company usually sells coins, and investors hope that the value of those coins will increase over time. It is important to mention that ICO happens before the public exchange listing. Buying ICO allows you to buy tokens at a better price before they are released for trading by the general public.

Security Token Offering

The second option is STO or Security Token Offering. The main problem with ICO is that an alarming number of companies have used it as a way of scamming investors. STOs, on the other hand, provided security instead of hope that the value will increase. Usually in the STO, the company offers a part of its business, profit, dividends, and even interest rates. Participating in an STO means that you are getting a part of the investment, which also includes security. So, whether you get partial ownership or borrowed money, you get something tangible in return, unlike in ICOs.

Initial Exchange Offering

IEO is a version of ICO which is administered by a crypto exchange on behalf of the company or a startup. The upside is that exchanges give more credibility to the projects that are participating in IEOs. IEO is a bit safer than the alternative, but it’s far from perfect. It is not rare that coins get distributed unevenly. This can lead to a small part of investors owning a majority of tokens, which will allow them to dictate the course of the market and manipulate the value.

Choosing a Development Team

Whether you have a clear idea or you are looking for inspiration, finding an experienced development team can be beneficial for your project. Consider finding professionals who already have experience in the blockchain world. Needless to say, assembling a good team won’t be cheap, but it might mean a difference between success and failure.

Outsourcing your development can have its perks, so before making a decision make sure to read our article comparing In-house vs. Outsource Blockchain Development.

Coin/Token Economics

Each coin is set up on its own blockchain, and as a result, it creates its own ecosystem. It’s nearly impossible to create a universal rule that determines the value of each of the coins. Also, neither tokens or coins are tangible. You can’t get your hands on a shiny new Bitcoin.

The first thing people think of when they hear about the origin of coins or tokens is inflation. In the example of Bitcoin, a new one is created approximately every ten minutes. But for a single miner, it might take years to solve a block. Since solving these puzzles can be quite problematic for a single node, miners decided to create mining pools. By connecting hundreds of miners into a pool, they have a better chance of solving a block and receiving the prize. The reward is then split equally between the pool members.

The value of tokens itself will increase when there is a higher demand for purchasing them. This means that if the number of people looking to buy a coin at a certain price is higher than the number of coins for sale, the price will grow.

While the regular economy and fiat money have been around for centuries, digital money is a bit over a decade old. There hasn’t been enough time or research to accurately describe everything that has happened since Bitcoin appeared in 2009. Chris Burniske did an incredible job with his valuation of altcoins, so be sure to check it out if you want to know more about this new type of economics.

Define Technical Specifications

When you decide which type of currency you want to create, you will have to define technical specifications. For example – when creating tokens, you will need a lot less time and money to invest, and the whole process is rather simple. Not only do you not have to be an expert in programming, but you can follow simple steps to get the desired results.

On the other hand, creating coins requires you to design nodes, create a new blockchain, and so on.

Consensus Mechanisms

Although there are many cryptocurrencies out there, more or less they are all based on the same principles. Each altcoin that’s based on blockchain will have to validate which transaction is valid and which is not. One of the things that can make altcoins unique is the way they reach consensus.

Consensus mechanisms are algorithms and protocols that ensure that all nodes in the network are synchronized and that they agree on the legitimacy of transactions. A blockchain would not be able to work properly without a functioning consensus mechanism.

Among the most popular mechanisms are PoW, PoS, and PoA, as previously mentioned. The proof-of-work is also the first mechanism ever, and Bitcoin started using it in 2009. Many other altcoins have followed the example since. The PoW process is what is commonly known as mining. Nodes or miners have a goal of solving a complex puzzle, and the first one to do it will create a new block. Interestingly, these complex puzzles are quite difficult to solve but easy to confirm once the answer is found.

The only way to solve the puzzle is by guessing the right answer. If you imagine a padlock with a code, the only way to open it is by randomly guessing the number. There is no easier way to open it, but once you do, it’s quite easy to confirm that the number you have is the right one. Naturally, mining is a lot more complex. The faster the blocks are solved, the harder the puzzles are. Finally, if miners are looking to increase the speed of solving, they will have to invest in more computing power, which can get quite expensive.

Costs of Creating a Cryptocurrency

The first important thing to decide when determining the cost of making your own cryptocurrency is whether you want coins or tokens. As we mentioned, tokens use a pre-existent blockchain, and you create your own token on top of it. For example, if you build your token on ERC-20 standard it will be created on the Ethereum network, and you will have to pay in Ethers to do so.

Here’s a comparison of coins and tokens:

When it comes to creating coins, that’s a bit more complicated. In theory, creating your own altcoin is free. However, the process is significantly more difficult than the alternative. Unless your coding skills are impressive, this can prove to be quite challenging. You will need to find an expert (or a team of experts) to do it for you, which can be costly.

Finally, you can fork a coin, which still requires experience and knowledge about blockchains and programming.

Make Your Cryptocurrency Legal

When it comes to the legality of altcoins, the law varies from state to state and from country to country. There are countries like the U.S. where Bitcoin and similar altcoins are considered as both currency and security. In Mexico, Bitcoin is a virtual asset. In countries like Algeria, Egypt, Morocco, and several other cryptocurrencies are considered illegal. Russia, for example, allows mining but not banking. And the Bank of Montreal has announced that it will ban both debit and credit card users from any purchases related to altcoins. As it stands right now, the countries that are leading the way when it comes to regulating cryptocurrencies are Lichtenstein, Switzerland, and Malta.

There are many states without any laws regarding digital currency, but that may change soon. Be sure to check what your country’s laws say about this and try to prepare yourself for potential changes in regulations. The last thing you need is an unexpected surprise that can ruin your effort. A report by the Law Library of Congress mentions 130 countries and regional organizations that offer policies or laws regarding this subject.

The Technical Process of Building a Cryptocurrency

We will start with all the steps you’ll need to go through if you want to create coins.

Building Your Own Blockchain or Using the Existing One

One of the first things you can do is copy the code of Bitcoin, for example, add a new variable, and voilà — you have your own blockchain. While the process might last as little as five minutes, you should know how it works and what it does. Fully understanding the code behind the blockchain requires knowledge and skill, so it might be best to find an expert to help you with this task if you are not a programming pro.

Among the most popular blockchain platforms are:

- Ethereum – The platform was created in 2015, and it’s using a modified Nakamoto consensus that’s similar to Bitcoin’s. This consensus is in conjunction with the proof-of-work, and it’s featuring smart contract functionality. Ethereum also provides a decentralized virtual machine that can run scripts via a network of public nodes.

- Hyperledger Fabric – Hyperledger was launched in 2015, and the goal behind it was to improve cross-industry collaboration using developing blockchains and distributed ledgers. While initially people believed that the whole project will be based on Bitcoin, the director of Hyperledger announced that they will never build their own cryptocurrency. This project received support from Intel, IBM, and SAP Ariba.

- Multichain – The main idea behind the Multichain is to allow users to create private blockchains that they can later use for various transactions. This way, users can get their own blockchains with native currencies or assets.

- Waves – Waves have a similar goal like multichain. The platform is designed to help users create tokens instead of coins and blockchains. This way, they can skip the whole designing part if they are interested in end-result only. Users can later trade new tokens on Waves’ decentralized exchange.

- Ripple – Ripple is a payment protocol with the goal of enabling transactions almost anywhere in the world. The platform supports tokens that are representing fiat currency, cryptocurrency, and many other units of value like commodities and even mobile minutes.

- OpenChain – OpenChain is an open-source distributed ledger. The platform is designed to enable various organizations that are looking to issue and manage digital assets. All transactions via OpenChain are instant, there are no additional fees for miners. However, OpenChain doesn’t use blocks, and each transaction is directly chained to one another. This way, there is no time lost because there is no waiting period for blocks to be created. OpenChain is a more transactional chain than blockchain but utilizes the same ideas and values.

The blockchain you should use is based on the consensus mechanism you pick. It should be the one that suits your business idea best.

Designing Nodes

Once you have picked the right blockchain platform, you can proceed to create nodes. These are devices that are connected via the internet to your platform. They have the goal of completing specific tasks, such as verifying transactions or store data.

One of the things you need to decide on is whether the blockchain will be private, public, or in between. A public blockchain, or permissionless one, is a platform where anyone can join, read and write on the blockchain. On the other hand, private blockchains or permissioned ones, are networks with restrictions on who can participate in network and transactions. You will need to pick an operating system that nodes will use such as Windows or Ubuntu. Any OS can be used for blockchain, so you can pick the one you’re most comfortable with. If you are experienced with using Windows, you will have no problems setting up everything and tweaking it. However, Linux can be more stable when running 24/7.

Finally, another important aspect is hardware requirements such as processor speed, GPU, disk space, memory, and so on.

Blockchain Architecture

Blockchain architecture consists of a series of parameters you need to set before the launch. You need to set nodes, block sizes, rewards for validating blocks, and so on.

So be careful and thorough when doing this part since it might be essential for the performance of your blockchain.

Integration of APIs

Now, assuming that you have already picked a platform, you should understand that not every one of them offers API or Application Programming Interface. But even if your platform doesn’t offer a pre-built API, there is nothing to worry about. The good news is that you can easily find an API provider for your blockchain. The main goal of API is to deliver various data and establish a connection between programs and devices.

If your desired blockchain doesn’t offer API, you can try one of the following providers:

- ChromaWay

- Bitcore

- Blockchain APIs

- Factom Alpha API

- Gem

- Tierion

- Neurowave

- BlockCypher

- Colored Coin APIs

- Colu

User Experience

User experience is one of the key stumbling points on the road to the mass adoption of cryptocurrencies. It won’t do you any good to have the best cryptocurrency in the world and a bad interface. You will also need an interface design both for users and admins. So spending an extra buck on design would be a good move.

Your main goal when it comes to the interface is to enable users to understand everything that’s happening and can intuitively use your application.

Forking as an Alternative Way to Create a Cryptocurrency

We have already briefly mentioned forking before, and now, we will go into more detail about this alternative way of creating coins.

What Is Forking?

Ever since Bitcoin appeared a decade ago, blockchains have been growing and improving. Talking about software, there will be inevitable updates. Similarly to how you get an update on your smartphone, the network itself will undergo changes in its lifetime. Each and every node in the network runs on the same version of the software. Forking can bring an important update to the network or be used to create a “copy” of the existing coin with the same or different parameters. Usually, forks will bring a new update to it, and all nodes will switch to this newer version. For example, Litecoin is a forked version of Bitcoin, where certain changes were made to make it 4x faster and a total coin supply was set to 84 million, compared to Bitcoin 21 million.

But, forking is also sometimes used to revert to the older version of the software in case of hacking or malware. This way, instead of fixing the error or problem, the blockchain will simply revert to the previous state when everything worked properly.

Sometimes, forks can be the result of some disagreement within the community too.

The Difference Between Hard and Soft Fork

There are two types of forks — soft and hard. As all nodes work on the same version of the software, it is possible to have a disagreement on whether or not they should switch to a newer version. In this case, a part of participants will switch to a newer update, while the rest will remain on the older version, causing a permanent split in the blockchain. This is a hard fork. The first part of the community will continue operating on the older version, while the new one will work using the newer one. In essence, this will create a new cryptocurrency, independent of the previous one.

The one example everyone knows about is a split between Bitcoin and Bitcoin Cash. In 2017, miners and developers were trying to find a way to improve Bitcoin. They suggested an increase in the size of each block, allowing for more transactions. A part of the community refused to accept this term, and it resulted in a hard fork. During this time, Bitcoin continued to work on the old protocol, while Bitcoin Cash had larger blocks with more transactions.

In this case, users operating on the old version are no longer able to accept transactions from the newer version. Hard forks need between 90% and 95% of nodes, and all nodes running an older version won’t be accepted anymore.

The other type of forking is known as soft, where some users will still stay on the older protocol, but they can participate in accepting transactions from the newer block. They can choose to update at any point, but it is not mandatory.

How to Fork a Coin

Bitcoin is an open-source protocol, which means that anyone can take the code, add a few changes, and they will have a new coin. It takes little to no skill to do it yourself. So are many other digital currencies. You can even find a service like ForkGen, which is a generator of fork coins. This way, you can change a few parameters and create your own variation of a certain coin.

Of course, you can do this the harder way as well. If you are looking to test your skills, go to GitHub and compile the code for Bitcoin on your PC. The next step is to reconfigure all the changes and additions you want in your new altcoin, and after you’re done programming, publish it back on GitHub.

While it might seem unreal, there are several successful forks of Bitcoin that are currently on the market. They have managed to use the name and capital of the older sibling but create their own name in the process. These forks are Litecoin, Bitcoin Gold, and Bitcoin Cash.

How to Create a Token

A step-by-step guide for creating your own token is quite simple. All you have to do is select the platform you want to use and copy the protocol for creating tokens. After that, you will need to change a few parameters like the number of tokens on the market, the name of your currency, decimal places, and so on. Of course, you will need to invest a bit before your tokens are on the market.

As soon as you finish setting up details and parameters of your tokens, your digital money will appear on the network. You can then transfer any number of units to any user on the network, others can buy tokens from you, and you’ll be ready to use it as any other cryptocurrency.

Popular Platforms for Token Creation

Here, we will take a look at the most popular platforms that you can use to create tokens.

- Ethereum

The popularity of Ethereum keeps growing, and it is the best-known platform after Bitcoin. Ethereum enables the building and running of DApps and Smart Contracts without any interference or third parties. In 2018, there were almost 30,000 nodes on the main network. If you are looking to build a token on this very platform, you will be able to complete it in no time. Ethereum offers the ERC20 standard for creating new tokens, and they will be available almost immediately on its network. Naturally, for launching your version of the ERC20 standard, you will have to pay Ethers. There are also newer versions of the standard such as ERC223, ERC721, ERC777, ERC1155, etc. - NEO

One of the great advantages of NEO is that it supports a wide range of programming languages. While they advise users to choose C#, you can also use Python, Go, Ruby, Java, JavaScript, C/C++, and many others. If you opt for this platform, you will base your token on the NEP-5 standard. Fortunately, with each of these tokens, there is a test network, so you can see if everything works before paying anything. This is important to mention since creating NEP-5 token will cost you 490 GAS, which can be over 1,500 USD. - Waves

If the last example scared you, Waves is here to make everything better. Creating a token using the Waves platform is both easy and cheap. It costs only 1 Waves to create a token, which is less than $1. You can choose the name, number of decimals, total supply, etc. The interface for creating tokens is user-friendly, and you won’t have to spend hours trying to make it work. - NEM

NEM works similarly to Waves. You will get both a great interface and low prices. The whole process will take a couple of minutes, and your token will be ready to use. The NEM platform uses Java as a programming language, and its main currency is XEM. However, the one you create can assume any name you want. - EOS

The basic principle behind EOS is similar to Ethereum. However, unlike Ethereum, there is no proof-of-work. Instead, EOS uses a delegated proof-of-stake, which means that they use delegates instead of miners. Interestingly, their idea is to provide commercial stability, flexibility, and equal opportunity. The EOS version of tokens is eosio.token, and you can use it as a template for creating your own digital money.

Steps After the Creation of a Cryptocurrency

Once you have finished making your new digital coin, there are several steps that you should consider making. Creating a token or coin is only part of the process, and there are more things you should cover before your business is ready.

Build a Community

Many suggest that the first thing you should do is start building a community. Your coin will be worthless if there is no one to use it. The market is quite competitive, and fighting for your place will not be an easy task. However, if you do it properly, you can build a powerful currency based on the trust and activity of your community. Your community will become your early adopters, and if you do well, your evangelists.

Now, building a community may sound simple, but it is, in fact, one of the most challenging tasks today. There are dozens if not hundreds of marketing agencies out there that all claim to be able to do “growth hacking” that will allow you to have thousands of loyal followers within weeks instead of months, and, most likely, years.

But, how do you properly build a community around your cryptocurrency?

Start Early

Did you decide to create a cryptocurrency? Well, the moment you decide to create it is the right time to start building your community and your brand image. Create accounts on Twitter, Facebook, LinkedIn, Quora, Medium, and Telegram. You have to have a presence everywhere, and you have to start right away. It doesn’t matter that all you have now is an idea. It doesn’t matter your logo isn’t quite there yet. It doesn’t matter your website has a few photos and a bunch of “Lorem ipsum”. Just start.

Engage

The days when it was enough to just show up online and say “I’ve done something cool” in order for people to flock around you are over and gone. Nowadays, in order to get people interested, you need to show interest first. You want crypto influencers to check out your cryptocurrency? Engage with them. Go to their posts, comment, ask, and respond. Sure, you have to know your stuff, but as soon as you enter some discussions, people will start checking you out, following you, checking out what you’re doing, and in the end following your company.

Be a Thought Leader

Well, not necessarily you, but one of your team members will have to take on the burden of being the brand face and mind. One of you will have to be loud and smart about everything that is going on in the crypto scene. Someone hacks Binance? BTC drops? ETH trouble? New blockchain emerging? Your company’s thought leader will have to tweet about it, comment for crypto news sites, post memes on Telegram, write a short blog, and engage in a discussion on LinkedIn regarding this topic. That way, you (or the designated thought leader of your company) will look like you know crypto inside and out like you see everything that is going on, and you have relevant insights to share. If you are a good thought leader, someone people recognize, you get credibility, and your company gets a ton of it by sheer association.

Learn Who Your People Are

You can enter a loud room and talk to everyone at once. No one will hear you, or pay any attention to what you’re saying, but you can do it. However, if you know that what you have to say is interesting to that group of jocks by the bar, you’ll walk over to them, and engage them in a conversation. And they’ll listen. The same goes for the crypto community. You have to know who is the target audience of your cryptocurrency. Millennials? Traders? Opportunists? Adjust your style of communication and the things you’re highlighting about your cryptocurrency to them, and they will respond. Why? Because they will believe you know who they are, and you will be speaking their language.

Make sure to create value for them

Just updating people on every step of your long and perilous journey towards creating a cryptocurrency isn’t enough for them to stick around and feel invested in your project. But, if you manage to create a story for them, make a show out of it, make them feel for your successes and failures, reward them when you’re doing well, and ask for their advice when you’re stuck, you’ll basically give them a reality show that they can earn from. And in this day and age, that is everything.

Plan Ahead

Many developers agree that the least time-consuming part of the process was creating the altcoin. Knowing how to create a digital currency is not the hardest part. You need to plan ahead and have a clear goal of what you want to accomplish. Each coin faces a different problem, and they all offer a solution. As we have mentioned, creating one is easy, but you want to make it last. If you are just looking to create one for the sake of it, you won’t have a great time. However, if you invest time and energy into making a perfect coin, you will enjoy what becomes out of it.

Get Validators Onboard

Validators (most commonly, miners, but not every coin comes from mining) or nodes are an important part of the crypto world. Once you have created something you like, you need to spread the word about it so that people want to mine it or otherwise come aboard. Not only will this improve the performance of your digital money, but it will also raise awareness, and it will pique interest. The more people hear about your coin, the more of them you’ll have onboard. As a result, its price will rise.

You need to understand that miners invest their resources. Today, most mining rigs use GPUs since they have proven to do the job better than CPUs, while spending less energy. However, these still cost a lot, and people are not willing to risk much. So keep in mind their expectations and needs as well.

Innovate and Improve Constantly

The whole cryptocurrency market is highly volatile, and it keeps changing. You need to change as well. Besides, you won’t get far if you stick to one principle and refuse to adapt. You should keep innovating and improving, and as a result, your business will thrive. If you find a group of like-minded people, they will support you.

Conclusion

While the whole market is rather young, it has already managed to make quite an impact on the whole world. People understand the potential and benefits that come from using altcoins, and the interest in it keeps growing. Since 2009, when Bitcoin launched, there have been over 6,000 different altcoins on the market.

So if you are looking for a hint or sign whether you should create your own coin, this is it. People from all over the world are learning more and more about this new digital money, and they love what they see. The very appearance of many different types and variations is proof of how much people want more. If you wanted to know how to make a digital currency, hopefully, you have a clearer image now. The only thing you need to do is take the right approach and make history. Maybe you will create an Ethereum token from the start, but in time, it might evolve into a coin or who knows? Remember that there are no limits in an industry as innovative as this one.